The global growth outlook 2026 is increasingly defined by weakening momentum across major economies. Growth downgrades are emerging simultaneously across advanced and emerging regions. As a result, analysts are shifting from recession forecasts toward concerns about prolonged stagnation. This synchronized deceleration suggests that the world economy is entering a phase of structurally weaker expansion rather than a short cyclical dip.

Importantly, the world economic outlook 2026 reflects overlapping constraints that limit recovery potential across regions. Weak demand, restrictive financial conditions, and geopolitical fragmentation are reinforcing each other. For broader context on slow growth, sticky inflation, and rising debt, see the EconomicLens analysis on the global economic outlook for 2025–2026 (https://economiclens.org/global-economic-outlook-2025-2026-slow-growth-sticky-inflation-rising-debt/).

Global growth outlook 2026

The world economic outlook 2026 shows a rare convergence of slowdowns across the world economy. Historically, weakness in one region was offset by strength elsewhere. That offsetting mechanism is now largely absent.

According to recent IMF projections (https://www.imf.org), global GDP growth is expected to remain below its pre-pandemic average. Moreover, successive forecast revisions continue to trend downward.

As a result, the dominant risk is prolonged low growth rather than a sharp contraction.

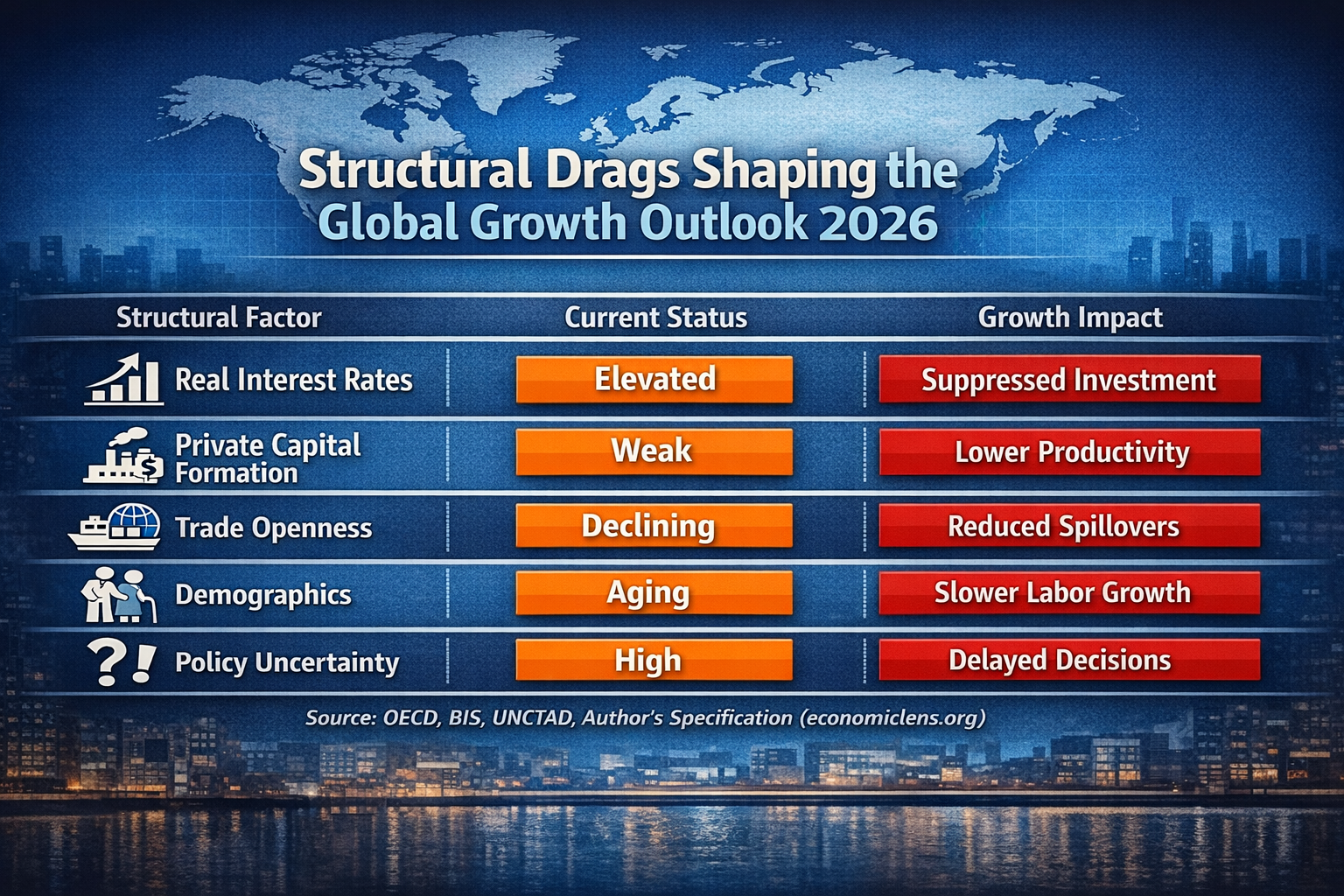

This table illustrates why the world economic outlook 2026 2026 reflects synchronized weakness rather than regional divergence.

Monetary tightening and its lingering impact on the world economic outlook 2026

First, monetary policy continues to weigh heavily on the world economic outlook 2026 2026. Although inflation has eased, interest rates remain elevated relative to historical norms.

High borrowing costs suppress housing, credit, and private investment. Even where policy easing begins, real rates are likely to remain restrictive. Consequently, demand recovery remains slow.

In addition, tight global financial conditions constrain emerging markets that rely on external financing.

Weak private investment and productivity constraints

Second, weak private investment is a defining feature of the world economic outlook 2026. Firms face uncertainty linked to trade policy, geopolitics, and regulatory fragmentation. Increasingly, fragmentation is becoming the default setting of the global economy, reshaping trade, supply chains, and capital flows (https://economiclens.org/fragmentation-is-now-the-default-setting-of-the-global-economy/).

At the same time, productivity growth remains subdued. According to the OECD (https://www.oecd.org), productivity gains across advanced economies are well below long-term averages.

As a result, potential growth is declining across regions.

These factors explain why the global growth outlook 2026 remains weak even without a crisis trigger.

Loss of a global growth engine

A defining feature of the world economic outlook 2026 is the absence of a clear growth engine. For much of the past two decades, global slowdowns were offset by rapid expansion in large emerging economies.

That mechanism has weakened. Structural pressures such as property-sector adjustment, demographic aging, and a shift toward state-led investment models have reduced global spillover effects. Although large-scale public investment programs may stabilize domestic output, they generate fewer external demand impulses.

Recent infrastructure pipelines and public spending initiatives illustrate this shift toward inward stabilization rather than outward-driven growth (https://economiclens.org/china-unveils-42-billion-project-pipeline-for-2026-growth-push/).

As a result, global demand lacks a dominant source of momentum.

For a broader discussion of how emerging economies fit into this changing landscape, see EconomicLens analysis on global growth leadership (https://economiclens.org/global-economic-growth-can-emerging-economies-challenge-chinas-economic-dominance/).

Trade fragmentation and erosion of export-led recovery

Another critical constraint on the global growth outlook 2026 is trade fragmentation. Sanctions, tariffs, and strategic trade restrictions are reshaping global commerce.

Export-led recoveries are harder to achieve. Trade barriers reduce efficiency and raise costs. According to UNCTAD (https://unctad.org), global trade growth has slowed significantly relative to GDP.

Consequently, trade no longer amplifies recovery across regions.

Fiscal constraints and rising debt pressures

Fiscal space is increasingly limited in the global growth outlook 2026. Public debt remains high following successive shocks.

Rising interest costs are crowding out productive spending. The BIS highlights that higher debt servicing burdens reduce fiscal flexibility (https://www.bis.org).

Therefore, governments face constrained policy options.

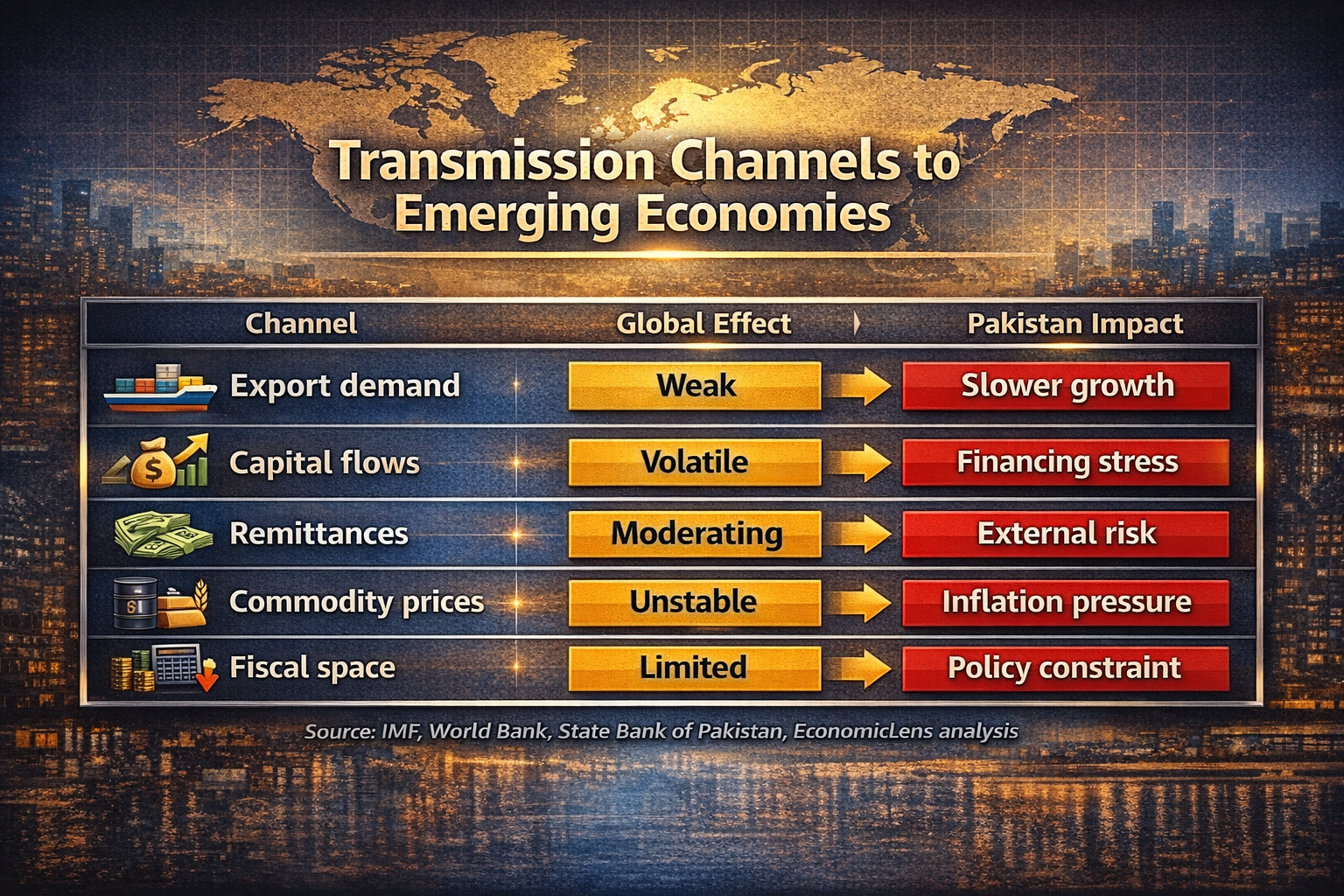

Implications for emerging economies and Pakistan

For emerging economies, the global growth outlook 2026 implies weaker export demand, volatile capital flows, and tighter financing conditions.

For Pakistan, these pressures translate into slower export recovery, softer remittance growth, and increased vulnerability to commodity price shocks. This global backdrop complicates inflation control and fiscal stabilization.

Policy priorities under the global growth outlook 2026

Escaping prolonged stagnation requires more than monetary easing. Structural reforms, productivity-enhancing investment, and trade coordination are essential.

Without addressing fragmentation and investment weakness, the global growth outlook 2026 is likely to remain subdued even if inflation stabilizes.

Conclusion

The global growth outlook 2026 reflects a world economy constrained by structural forces rather than temporary shocks. Weak demand, tight financial conditions, and fragmentation are slowing growth across regions simultaneously.

The central risk is not recession but stagnation. Navigating this environment will require rebuilding growth foundations in an increasingly fragmented global system.

1 thought on “Global Growth Slowdown 2025–2026: Are Major Economies Sliding Into a Synchronized Stagnation?”

I am pleased that I observed this web site, just the right info that I was looking for! .