Global water stress 2025 intensifies as canal bottlenecks, shrinking river levels and hydropower losses disrupt global supply chains. This blog explains how drought, shipping delays, energy shortages and climate-driven water scarcity reshape trade networks, manufacturing inputs and global logistics stability.

INTRODUCTION

The global water stress 2025 landscape reflects one of the most severe disruptions to global trade, energy systems and industrial supply chains in recent history. Prolonged drought, shrinking river levels and reduced canal throughput intensify pressure on global logistics at a time when markets remain sensitive to geopolitical tension and inflation risk. Consequently, the interaction between climate-driven water scarcity and high trade dependence amplifies systemic vulnerability across economies.

In the global water stress 2025 environment, major chokepoints including the Panama Canal, Rhine River, Yangtze River and Parana Basin experience restricted navigability. Meanwhile, declining hydropower output reduces energy availability across Africa, South Asia and Latin America, increasing reliance on expensive thermal imports. Additionally, manufacturing hubs face delays in raw material shipments as water dependent transport routes slow down.

This blog analyzes the drivers of global water stress 2025 through detailed climate indicators, canal bottleneck assessments, hydropower losses and cross-regional supply chain disruptions. Furthermore, it integrates expert insights, 2024–2025 report analysis and data-driven metrics to evaluate systemic risk transmission across global trade networks.

1. Rising Global Water Stress and Drought Intensification

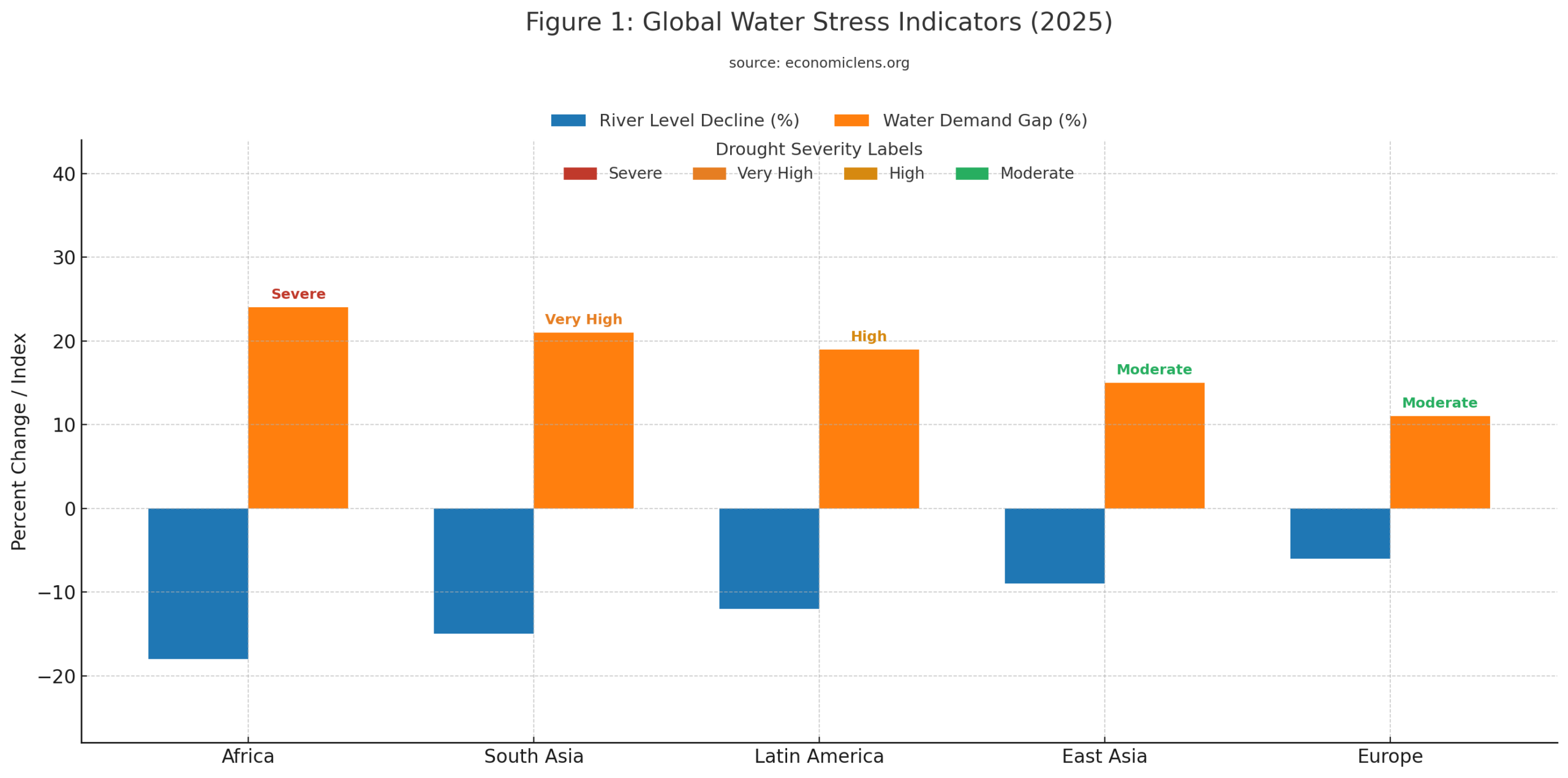

Global water stress 2025 intensifies as climate change accelerates evaporation, reduces rainfall and disrupts seasonal freshwater availability. Large regions across Africa, South Asia and Latin America experience acute shortages, increasing competition for agricultural, industrial and municipal water use. Consequently, water scarcity becomes a core driver of trade disruption, energy instability and food security risk.

Expert Insight & Global Report Signals: Drought and Structural Water Power Shifts

The UN World Water Development Report 2025 (https://www.unwater.org/publications/world-water-development-report) shows that declining river discharge now affects more than seventy major basins, sharply reducing freshwater availability for agriculture and industry. The IPCC Sixth Assessment Climate Indicators Update (https://www.ipcc.ch) confirms that rising evaporation and rainfall volatility intensify drought frequency across already stressed regions.

The FAO Drought Assessment and Food Production Outlook 2025 (https://www.fao.org) further links water scarcity to reduced yields and rising food production costs. Together, these findings signal a shift where control over resilient water systems increasingly shapes economic stability, trade competitiveness and food security outcomes rather than acting as a passive environmental condition.

Water stress indicators worsen across all regions as river levels fall and water demand outpaces supply. Consequently, agriculture, energy and industrial operations face rising constraints.

South Asia Faces Deepening Multi-Year Drought

South Asia experiences one of its worst drought cycles in decades, with India and Pakistan reporting critically low reservoir levels. According to national hydrological agencies, multiple river systems including the Indus, Ganges and Brahmaputra show severe depletion. Consequently, irrigation demand surges as temperatures rise, intensifying water scarcity and supply chain risk.

“Water stress grows fastest when climate pressure meets rising economic demand without sustainable replenishment.”

2. Canal Bottlenecks Under Climate-Driven Water Stress

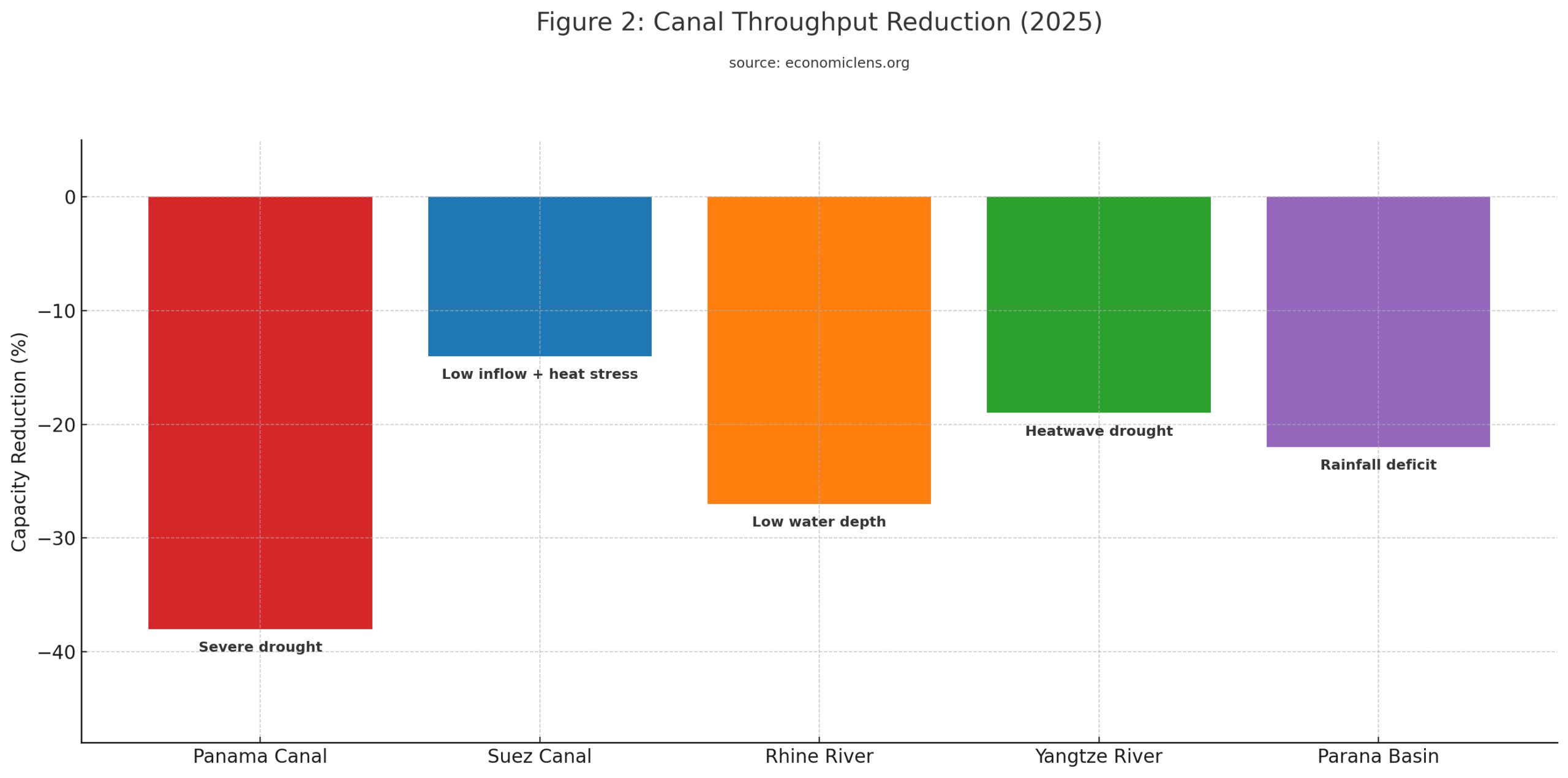

Canal bottlenecks become a defining feature of global water stress 2025 as major waterways face restricted capacity due to historically low water levels. These chokepoints constrain global shipping, lengthen delivery times and raise freight costs. Consequently, global trade routes experience delays that cascade across supply chains.

Expert Insight & Global Report Signals: Canal Bottlenecks and Maritime Trade Shock

The UNCTAD Maritime Transport Outlook 2025 (https://unctad.org) identifies climate-driven canal restrictions and conflict-linked chokepoints as one of the most severe structural risks to global trade. The World Meteorological Organization Hydrology Update 2025 (https://public.wmo.int) links prolonged drought to declining navigability across the Panama Canal, Rhine River and Suez-linked routes.

The IMF Trade and Inflation Diagnostic Notes 2025 (https://www.imf.org/en/Publications) warn that shipping delays and route congestion extend inflationary pressure by raising transport, insurance and inventory costs across global supply chains. This disruption aligns with wider geopolitical instability in critical maritime corridors. For a focused assessment of Red Sea instability and its spillover into canal traffic and global shipping, see (https://economiclens.org/red-sea-turmoil-suez-canal-disruptions-and-the-global-shipping-shock/)

These reports collectively illustrate how physical water shortages translate into logistical power, reshaping trade reliability and cost structures.

Throughput declines across critical channels as water levels fall. Consequently, shipping inefficiencies intensify global logistics strain and raise transport costs.

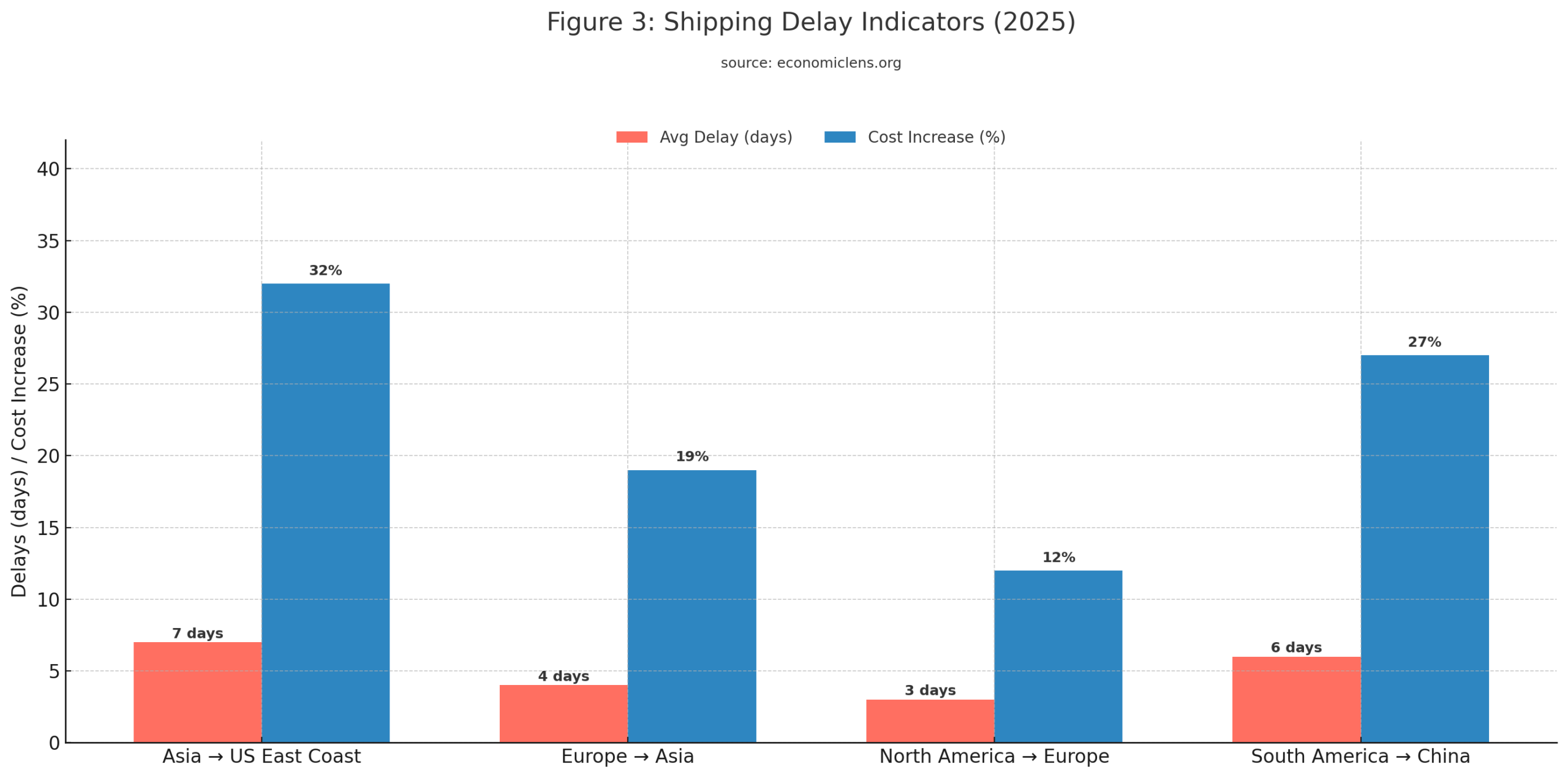

Shipping delays increase across major trade routes as canal restrictions widen. Consequently, delivery reliability declines and supply chain pressure rises.

Panama Canal Reduces Daily Ship Slots Again

The Panama Canal Authority imposes new restrictions on vessel slots due to critically low lake levels. According to Reuters, available crossings fall below 24 per day. Consequently, carriers reroute around Cape Horn or the US West Coast, increasing congestion and shipping costs.

“When water routes narrow, global commerce slows, raising the cost of distance for every economy.”

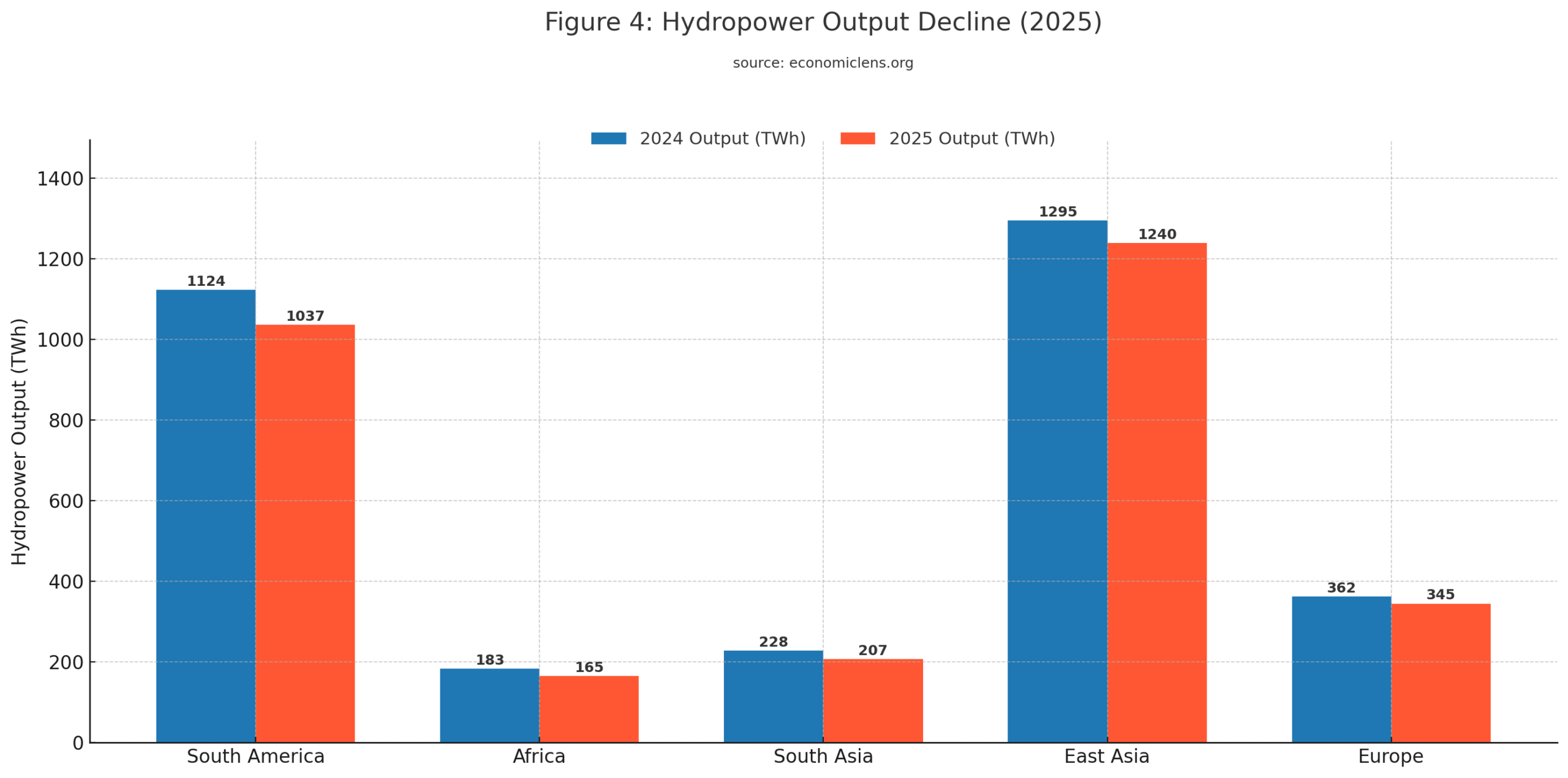

3. Hydropower Losses Caused by Global Water Stress

Hydropower output declines sharply under global water stress 2025 as reservoirs fall and turbine output weakens. Energy systems reliant on hydro generation face shortages, rising electricity prices and increased reliance on expensive thermal imports. Consequently, manufacturing hubs experience production interruptions and higher operational costs.

Expert Insight & Global Report Signals: Hydropower Losses and Energy Security Repricing

The IEA Electricity Market Report 2025 (https://www.iea.org) confirms that hydropower declines are now structural rather than cyclical due to persistent drought. The World Bank Energy Security and Climate Risk Assessment 2025 (https://www.worldbank.org) identifies water-linked power shortages as a key transmission channel into inflation and manufacturing slowdown.

The African Development Bank Energy Sector Outlook (https://www.afdb.org) reports acute electricity shortages in hydro-dependent African economies. For broader energy-economy implications, see (https://economiclens.org/global-energy-crisis-2025-power-shortages-policy-risk/)

Hydropower declines across all regions due to drought and low reservoir levels. Consequently, electricity shortages intensify and raise industrial production costs.

Brazil and Colombia Face Energy Strain From Low Reservoirs

Brazil and Colombia report significant reductions in hydropower due to multi-year drought cycles. According to the IEA, output falls sharply as reservoir levels hit record lows. Consequently, both countries increase thermal imports and face higher electricity prices.

“Energy reliability weakens when the rivers that power turbines fall faster than systems can adapt.”

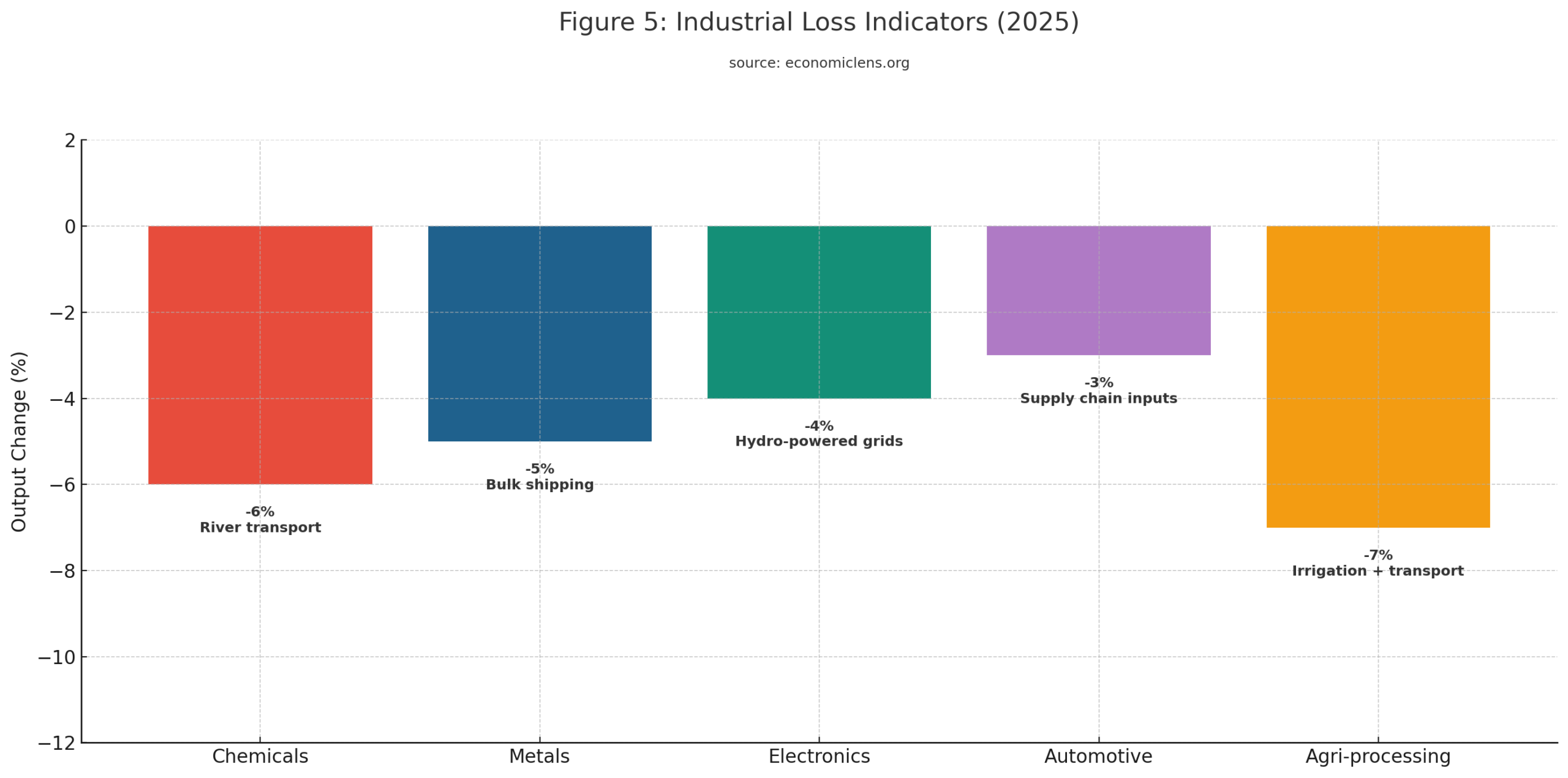

4. Supply Chain Vulnerability in an Era of Global Water Stress

Manufacturing supply chains face heightened disruption under global water stress 2025 as lower river levels restrict transport of bulk materials including chemicals, metals, grains, coal and fuel. Industries dependent on water-cooled processes and hydro-linked electricity face rising operational delays. Consequently, manufacturing output slows in water-dependent economies.

Expert Insight & Global Report Signals: Water Stress and Industrial Supply Chain Fragility

The UNIDO Industrial Development Outlook 2025 (https://www.unido.org) identifies water scarcity as an emerging structural constraint on manufacturing output and competitiveness. The OECD Inland Transport and Logistics Indicators 2025 (https://www.oecd.org) show rising vulnerability in river-dependent freight networks critical for chemicals and metals.

McKinsey Global Institute supply-chain research (https://www.mckinsey.com) highlights persistent cost escalation in water-dependent industrial processes.

Industrial output declines across key sectors due to transport restrictions and water-linked energy shortages. Consequently, production delays and cost pressures rise.

Europe’s Rhine River Disruption Slows Chemical Supply Chains

Low Rhine River levels restrict barge movement, delaying chemical and metals shipments across Germany and the Netherlands. According to BASF and other major firms, freight costs surge due to rerouting and reduced capacity. Consequently, European industrial production slows.

“Supply chains break down first where water meets industry and both begin to fail at once.”

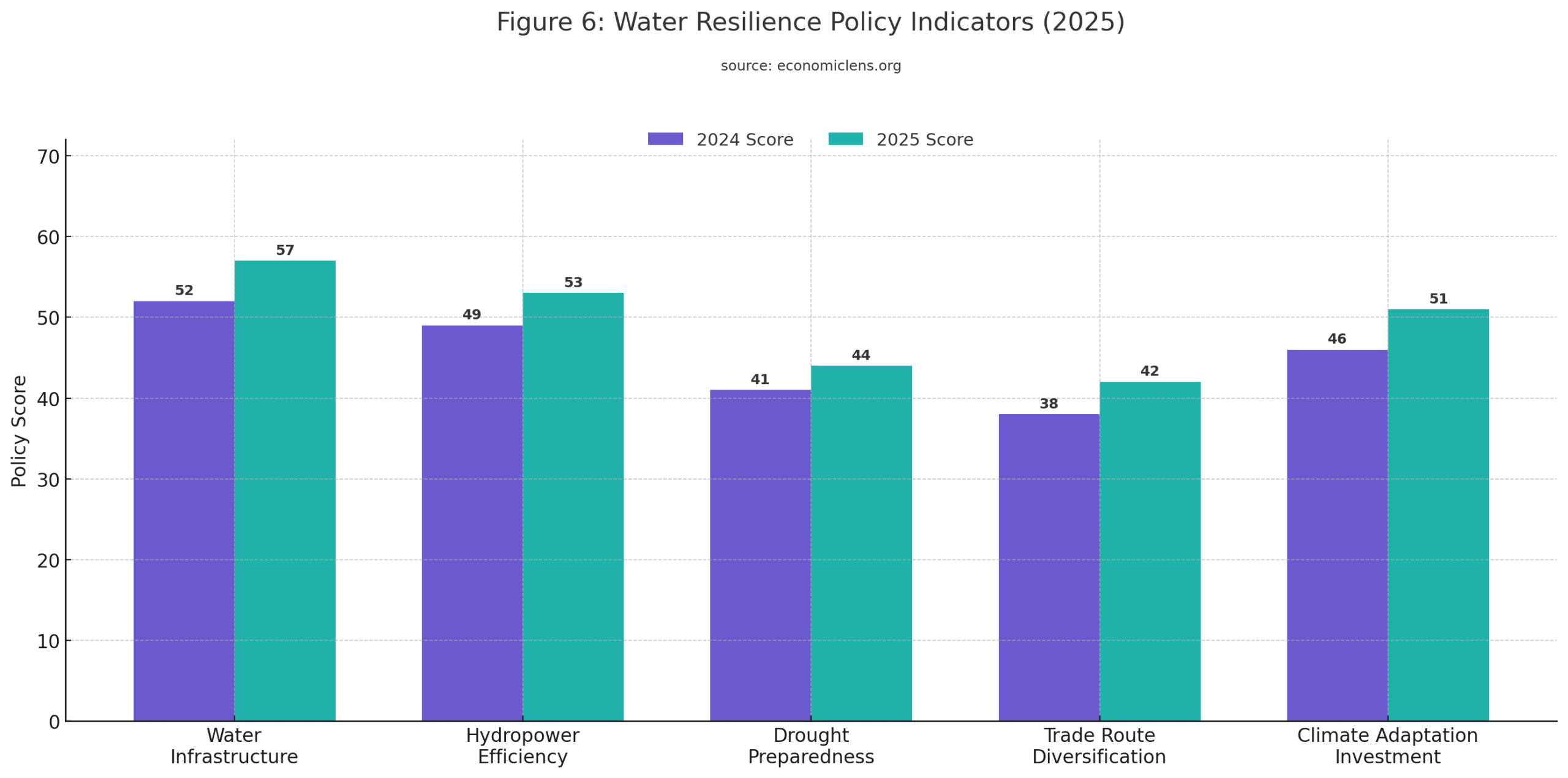

5. Managing Global Water Stress: Policy Gaps and Adaptation Risks

Global water stress 2025 accelerates long term adaptation challenges as economies confront uncertain rainfall patterns, rising evaporation and structural water scarcity. Policy responses require integrated planning across agriculture, energy, trade and infrastructure. Consequently, the global economy faces a prolonged adjustment period.

Expert Insight & Global Report Signals: Conflict-Driven Logistics Risk and Global Spillovers

The UN Global Adaptation Report 2025 (UNEP, https://www.unep.org) highlights that climate stress increasingly overlaps with geopolitical conflict, amplifying trade and infrastructure vulnerability. The OECD Global Trade Risk Indicators 2025 (https://www.oecd.org) show that chokepoint disruptions create cascading effects across food, energy and manufacturing supply chains.

The IMF Global Financial Stability and Trade Risk Notes 2025 (https://www.imf.org/en/Publications) further warn that prolonged maritime insecurity can translate into persistent inflation, capital flow volatility and fiscal stress for import-dependent economies.

These dynamics are already visible in conflict-affected shipping lanes. For a deeper examination of how Red Sea disruptions transmit into global inflation and supply-chain instability, see

(https://economiclens.org/red-sea-shipping-crisis-global-trade-fallout-inflation-pressure-and-supply-chain-turmoil/)

Policy indicators improve modestly but remain insufficient to counter rising water stress. Consequently, long term water security risks persist.

China Expands Water Diversion Projects to Protect Industrial Zones

China accelerates major water diversion efforts to sustain manufacturing hubs affected by Yangtze River depletion. According to national planners, new projects aim to stabilize industrial output. Consequently, China illustrates the scale of infrastructure required for adaptation.

“The future of global trade depends on how nations adapt when the world’s water runs low.”

Conclusion

Global water stress 2025 emerges as a defining risk for global supply chains, trade networks and energy systems. Drought intensification, canal bottlenecks and hydropower decline create structural disruptions across regions that remain deeply dependent on water-linked transport and electricity. Manufacturing hubs and agricultural exporters face rising delays and declining productivity due to transport constraints and water scarcity. Meanwhile, energy systems reliant on hydropower confront shortages that raise production costs and weaken economic stability. Although governments pursue adaptation strategies, current measures remain insufficient to offset long term climate-driven water pressures. The global economy therefore enters a period of heightened fragility where water constraints reshape logistics, industrial output and trade competitiveness.

Call to Action

Governments, industries and global institutions must prioritize water resilience strategies, diversify trade routes and invest in adaptive infrastructure. Long term economic stability will depend on timely action to manage intensifying water scarcity.

“Water stress will define the next era of global logistics. Economies that invest early in resilience will secure stability while others struggle to adapt.”

Analysis Note: This blog is based on independent analysis of publicly available information and data.